Check requirements for Asia's Retirement Visas

Singapore Retirement Roadmap: Maximise CPF & Other Income After 65

Navigate your golden years with confidence. Our guide breaks down how CPF LIFE, personal savings, investments, and property can form a multi-source retirement income plan for Singaporeans after age 65.

RETIREMENT PLANNINGSINGAPORE

9/8/20255 min read

So, you're approaching your golden years, and the big 6-5 is just around the corner. For many of us in Singapore, this is a significant milestone, a moment to finally slow down, enjoy life, and perhaps, for the first time in decades, stop worrying about the daily grind. But let’s be honest, the idea of "retirement" can feel a little daunting. The big question on everyone's mind is: "Will I have enough?"

I remember having this conversation with my own father a few years ago. He had spent his entire life working hard, saving diligently in his CPF, and raising a family. But even he, a man who planned everything with meticulous care, felt a pang of uncertainty. He knew he had his CPF savings, but he wasn't entirely sure how they would translate into a sustainable, lifelong income stream. And what about everything else? His savings, a small investment portfolio, the rental income from an old shophouse… how would it all fit together?

This article is for all of you who share that same quiet concern. It’s not about complex financial jargon or intimidating calculations. It's about breaking down the CPF system after 65 into a simple, friendly concept, and then looking at how your other income sources—your savings, your investments, and even your property—can work together to create a robust and worry-free retirement.

(It's scary not knowing what kind of income we will have in retirement. Use our Personal CPF and Income Planner to see how your income will look like when you are retired and have no more income!)

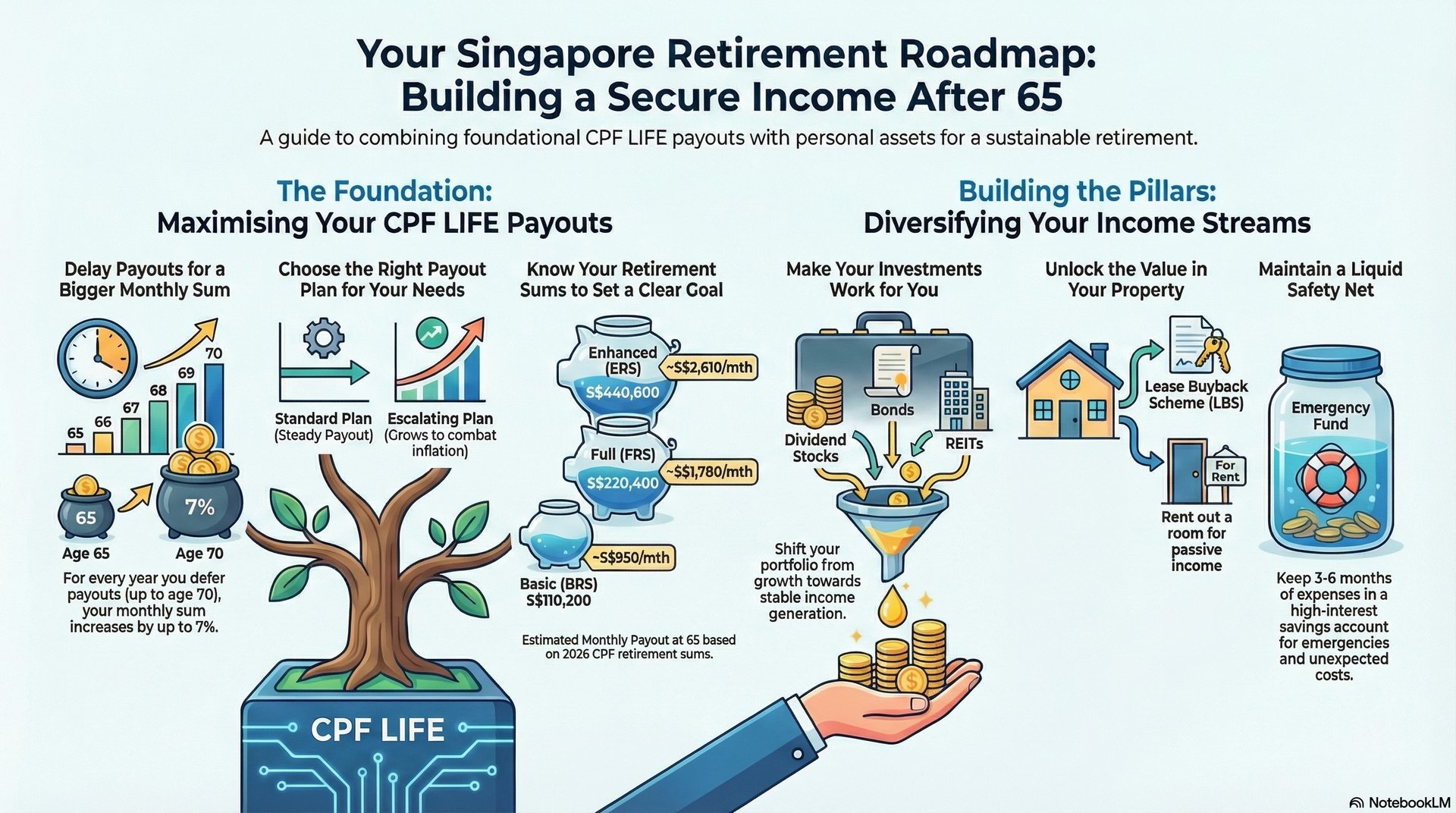

The Foundation: Decoding Your CPF Payouts at 65

Think of your CPF as the bedrock of your retirement plan. At age 55, a Retirement Account (RA) was created for you, with savings from your Ordinary Account (OA) and Special Account (SA) transferred over. Then, at age 65, you enter the CPF LIFE scheme, which is the key to a lifelong income.

CPF LIFE (Lifelong Income For the Elderly) is a national longevity insurance annuity scheme. In simple terms, it's a program that gives you a monthly payout for as long as you live, no matter how long that is. This is crucial, because with Singaporeans living longer, the biggest fear is outliving your savings. CPF LIFE takes that worry away.

You have some key decisions to make around age 65:

When to start your payouts: You can choose to start anytime between age 65 and 70. Here’s a little secret: deferring your payouts can be a powerful strategy. For every year you defer, your monthly payout increases by up to 7%. If you're still working or have other income streams, delaying your CPF payout until 70 could give you a much larger sum for the rest of your life.

Which plan to choose: CPF LIFE offers three different plans. Your choice should align with your lifestyle and how you feel about rising costs over time.

The Escalating Plan: Payouts start lower initially but grow by 2% annually for life. This is a great choice if you're concerned about inflation eroding your purchasing power over the years.

The Standard Plan: As its name suggests, this plan provides a steady, consistent monthly payout. It starts with a higher payout than the Escalating Plan, but the amount doesn't change, so you'll need to be prepared for the cost of living to potentially outpace your income.

The Basic Plan: This is a legacy plan that provides the lowest monthly payouts. The payouts will decrease over time as your CPF balances are drawn down. Most members will find the Standard or Escalating plans more suitable for their needs, but the Basic Plan can be an option for those with a very modest lifestyle.

Building the Pillars: Adding Your Other Income Streams

While CPF LIFE provides a reliable foundation, a truly comfortable retirement is built on multiple pillars. A good "Retirement Roadmap" is like a diversified portfolio of income sources, each serving a different purpose.

Your Savings: This is your liquid cash, the emergency fund for unexpected expenses or that last-minute flight to visit the grandkids. Keeping a portion of your savings in a high-interest savings account or a fixed deposit is a great way to ensure easy access while still earning a little something.

Your Investment Portfolio: This is where you put your money to work. For those in or nearing retirement, the goal of investing often shifts from aggressive growth to generating stable income. Consider a portfolio that includes:

Dividend-paying stocks: These can provide a regular stream of income.

Bonds or Singapore Savings Bonds (SSB): These are generally lower risk and can be a good source of consistent interest income.

REITs (Real Estate Investment Trusts): These are a way to earn income from properties without owning them directly.

Your Property: For many Singaporeans, their home is their biggest asset. It can also be a powerful tool for retirement income.

The Lease Buyback Scheme (LBS): If you're an HDB flat owner, you can sell part of your flat's lease back to HDB and use the proceeds to top up your RA. This boosts your CPF LIFE payouts while allowing you to continue living in your home for life.

Renting out a room: If your living situation allows, renting out a spare bedroom can provide a consistent and easy source of passive income.

Mapping It All Out: A Simple Plan Based on Your Age and Lifespan

It can be hard to visualize all this, so let’s put it into perspective. Your plan should be dynamic, changing as you get closer to retirement.

For the 40-50 year old: Your focus should be on building a strong foundation. This means maximizing your CPF contributions (voluntary top-ups are a great idea) and starting a diversified investment portfolio. You have time on your side, so a higher-risk, growth-oriented portfolio is suitable.

For the 55-65 year old: This is the time to consolidate and de-risk. You should begin shifting your investment portfolio from growth to income. Use CPF's Retirement Sum Scheme to project your future payouts and identify any potential shortfalls. This is the time to make those strategic decisions, like whether to defer your CPF LIFE payouts.

For the 65+ year old: You are now in the "payout" phase. The focus is on drawing down your various income streams strategically to fund your lifestyle. Use your CPF LIFE payouts for essential expenses and a portion of your investment income for discretionary spending and "wants." Revisit your budget regularly to ensure you're on track.

Planning for retirement is a personal journey. There's no one-size-fits-all solution, but by understanding the core components—CPF, savings, investments, and property—you can build a roadmap that feels secure and tailored to your unique needs.

Let's Talk!

What does your ideal retirement look like? Do you have questions about your CPF or other income sources? Share your thoughts and let’s discuss them!

Complete Singapore CPF accounts review

Toe to toe comparison between Malaysia's EPF and Singapore's CPF System

Singapore Retirement Roadmap laid out

Singapore Retirement Secret that the government doesn't want you to know!

This article is for informational purposes only and does not constitute financial advice. Consult a qualified financial professional before making any financial decisions, as investments and strategies involve risk.

Address

Blk 8 Cantonment Close

SIngapore