Check requirements for Asia's Retirement Visas

The "3M" Pillars of Singapore Healthcare: Explained for Beginners (MediSave, MediShield Life, MediFund)

Confused by MediSave, MediShield Life, & MediFund? Get a simple breakdown of Singapore's "3M" healthcare financing system, how each pillar works, and how they protect you from huge medical bills.

SINGAPORERETIREMENT PLANNING

11/6/20254 min read

Have you ever looked at a Singapore hospital bill and felt like you needed a finance degree just to understand it? Between the subsidies, the savings, the insurance, and the safety net, it can feel like a financial alphabet soup. But here’s a secret: Singapore’s famous healthcare model isn’t built on endless complexity—it’s built on three simple, distinct pillars known as the 3Ms: MediSave, MediShield Life, and MediFund.

Think of it like a three-layer birthday cake: one layer is your personal savings, the next is universal insurance, and the top is the government's safety icing. Understanding these three pillars is the key to managing your healthcare costs in Singapore.

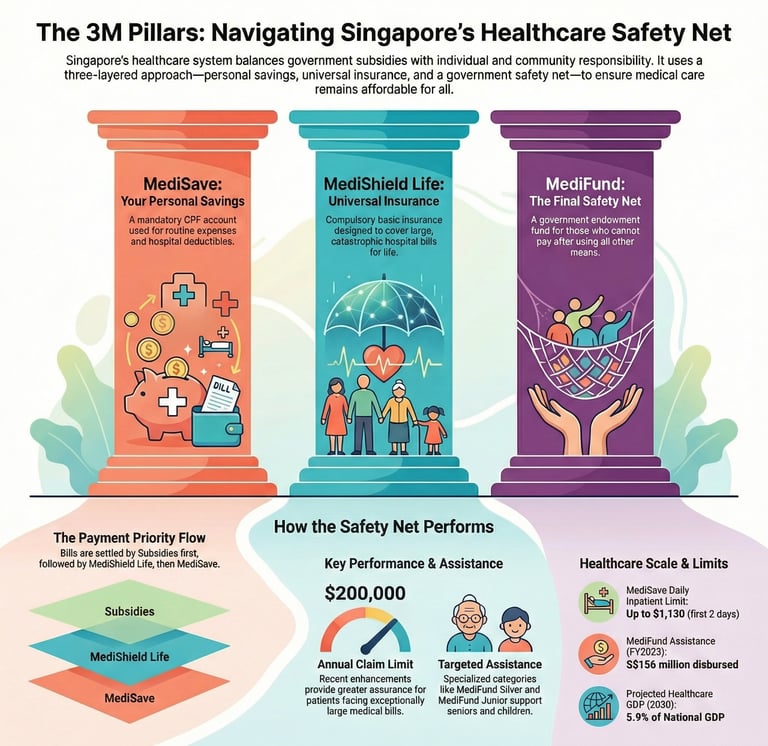

Pillar 1: MediSave (The Personal Savings Account)

What it is: MediSave is a mandatory personal savings scheme that is part of your CPF (Central Provident Fund) account. It’s essentially your dedicated healthcare piggy bank.

How it works: A portion of your monthly income is automatically contributed to your MediSave account. This isn't insurance; it's your money, and you can use it to pay for your own medical needs, or those of your immediate family.

The Role it Plays: MediSave is designed to cover routine, smaller expenses and the deductibles/co-insurance portions of large hospital bills. It reinforces the core philosophy of individual and family responsibility—you save for your own expected medical needs.

I remember when my dad had a minor day surgery. Instead of scrambling to pay cash, we simply used his MediSave balance. It felt incredibly reassuring to know that years of responsible saving were covering the bill automatically.

Key Use Limits:

You can use up to $1,130 per day for the first two days of an inpatient stay, and $400 per day thereafter for daily hospital charges (Source: CPF, March 2025).

It covers premiums for your MediShield Life and Integrated Shield Plans (up to withdrawal limits).

It has limits for specific procedures, like surgeries and chronic disease treatments.

Pillar 2: MediShield Life (The Universal Insurance)

What it is: MediShield Life is a compulsory, universal, basic health insurance plan. Unlike MediSave, this is a risk-pooling mechanism. Everyone contributes premiums, and the fund pays out for those who get hit with big bills.

How it works: Every Singapore Citizen and Permanent Resident is automatically covered for life, regardless of age or pre-existing conditions. Premiums are typically paid from your MediSave account.

The Role it Plays: MediShield Life is your protection against catastrophic illnesses—the high-impact, low-frequency events. It's designed to cover large hospital bills and selected costly outpatient treatments like chemotherapy and kidney dialysis.

A Crucial Data Point: Singapore’s national health expenditure is relatively low compared to other developed nations, with public and private healthcare expenditure projected to account for around 5.9% of GDP by 2030 (Source: International Trade Administration, 2025). The 3M system is a key reason costs remain contained, as it balances government subsidies with individual responsibility.

Coverage Details:

It covers bills sized for Class B2/C wards in public hospitals. If you opt for a private hospital or Class A/B1 ward, your payout will be lower proportionally, and your out-of-pocket costs will be higher.

Enhancements have increased policy year claim limits to S$200,000 to provide greater assurance for patients with exceptionally large bills (Source: Ministry of Health, October 2024).

Pillar 3: MediFund (The Final Safety Net)

What it is: MediFund is a government endowment fund of last resort. It is the final safety net for Singaporeans who are genuinely unable to pay their remaining medical bills.

How it works: It is not an entitlement. Patients who have exhausted all other means—Government Subsidies, MediSave, and MediShield Life—can apply for assistance through the Medical Social Workers at a MediFund-approved institution.

The Role it Plays: This pillar ensures that no Singaporean is denied appropriate, subsidised healthcare due to an inability to pay. MediFund Silver and MediFund Junior are carved out to provide more targeted assistance for seniors and children.

Impact and Scale:

In the Financial Year (FY) 2023 (April 2023 to March 2024), MediFund disbursed S$156 million in assistance to needy Singaporeans, across approximately 1.1 million successful applications (Source: Ministry of Health, November 2024).

Putting It All Together: The Financial Flow

When you receive a hospital bill in Singapore, the payment process typically happens in this order:

Government Subsidies: The bulk of the bill is reduced by government subsidies (this is why the official framework is the S+3M system).

MediShield Life: The insurance plan kicks in to cover the bulk of the remaining large, catastrophic portion of the bill.

MediSave: Your personal savings are used to cover the deductible, co-insurance, and any other MediSave-eligible portions.

Cash: The remaining small portion is paid in cash.

MediFund: If you still cannot afford the remaining cash payment, you apply to MediFund as a last resort.

The entire system is designed to share the cost across three parties: the Individual (MediSave), the Community (MediShield Life), and the Government (Subsidies and MediFund). That’s how Singapore keeps healthcare accessible and prevents medical debt from becoming a life-altering event.

Are you a Singaporean who has successfully navigated the 3Ms for a large bill? Share your experience in the comments below! If you found this guide helpful, please share it with others who are looking to understand their healthcare financing.

Complete Singapore CPF accounts review

Toe to toe comparison between Malaysia's EPF and Singapore's CPF System

The complete Singapore Retirement Roadmap

Singapore CDC cash voucher scheme

Singapore Retirement Secret that the government doesn't want you to know!

Disclaimer: This article is for informational purposes only and does not constitute professional financial or medical advice. Please consult with a qualified financial advisor or a Medical Social Worker for personalized guidance.

Address

Blk 8 Cantonment Close

SIngapore