FREE AI Analytics Tool for Health Reports and Scans available.

What is Singapore's CPF? A Simple Guide to the 4 Mandatory Accounts (OA, SA, MA, RA)

Confused about Singapore's CPF? This simple guide explains the 4 mandatory accounts (OA, SA, MA, RA), their uses (housing, health, retirement), and how they grow.

SINGAPORERETIREMENT PLANNING

11/4/20253 min read

Singapore old age retirement schemes has always consistent rank high in world's ranking. How do they do it? Here's a simple breakdown of a complicated scheme, if you will.

If you’re a Singapore Citizen or Permanent Resident, you’re looking at the Central Provident Fund (CPF). For many, the CPF seems like a mysterious black box—a mandatory savings plan that chews up a big chunk of their income every month. My wife, when she first moved here, thought it was just a giant tax! But trust me, the CPF is far more valuable and complex than a standard pension scheme. It’s actually a multi-purpose financial safety net designed to cover the three biggest costs of living in Singapore: housing, healthcare, and retirement.

Think of the CPF as a personal financial safety locker that automatically diversifies your savings across different life stages. When you and your employer make those monthly contributions, the money doesn’t go into one big pot; it is instantly split into different accounts, each with its own purpose, rules, and interest rate.

Let's break down the four mandatory accounts that manage your financial life here.

The 4 Pillars: Understanding Your CPF Accounts

Your CPF savings are allocated into three main accounts when you are under 55 years old: the Ordinary, Special, and MediSave Accounts. At age 55, a fourth, the Retirement Account (RA), is automatically created.

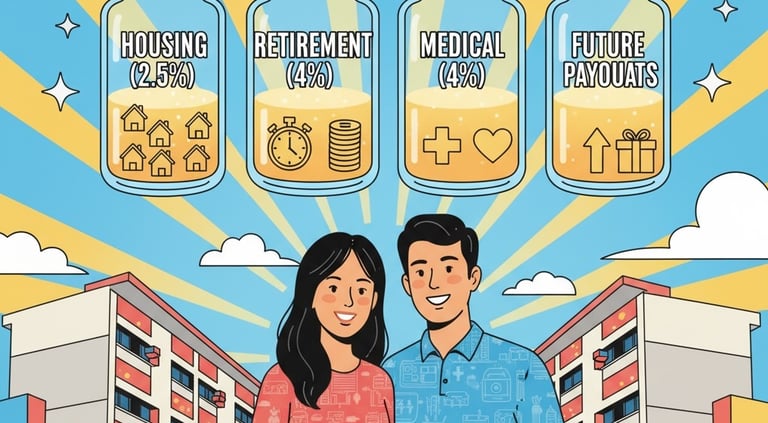

1. Ordinary Account (OA): The Housing & Education Hub

The OA is your most liquid and flexible account, but it's often the one with the lowest guaranteed interest rate at 2.5% per annum (as of Q3 2024).

Primary Use: Housing. This is where most Singaporeans tap their CPF to pay the down payment and service the monthly mortgage installments for their flat or private property.

Other Uses: Approved investments, education loans, and insurance premiums.

Relatable Anecdote: I remember when I bought my first HDB flat. That moment you sign the papers, and the agent says, "Okay, the down payment is covered by your OA," you suddenly appreciate that a big, difficult payment was actually saved up automatically for you over years.

2. Special Account (SA): The True Retirement Nest Egg

The SA is the CPF's long-term savings bucket, dedicated solely to your old age. It offers a higher guaranteed interest rate, currently 4.08% per annum (as of Q3 2024), which makes a huge difference over decades of compounding.

Primary Use: Retirement. Funds in the SA can only be used for retirement-related investments or, critically, they are locked away until retirement age.

Key Feature: Its higher interest rate means many financial planners recommend topping up the SA if you have spare cash, as it offers a high, risk-free return.

3. MediSave Account (MA): The Healthcare Safety Net

The MA ensures you have sufficient funds for medical needs. This is one of the most critical aspects of the CPF, designed to prevent citizens from facing crippling healthcare debt.

Primary Use: Hospitalisation, day surgery, certain outpatient treatments, and paying premiums for government-mandated health insurance like MediShield Life.

Contribution Cap: Contributions flow here until your balance reaches the Basic Healthcare Sum (BHS), which is set at $71,500 for those under 65 in 2024. Any excess is automatically channeled into your SA (or RA, if you are 55 and above).

4. Retirement Account (RA): The Payout Engine (Age 55+)

The RA is not funded by monthly contributions; it is created on your 55th birthday.

Creation: Money from your SA and a portion of your OA savings (up to the Full Retirement Sum) are transferred here.

Purpose: The funds here are primarily used to join CPF LIFE, Singapore’s national annuity scheme, which provides you with a guaranteed monthly payout from age 65, for as long as you live.

A Look at the Numbers

The beauty of the system is the forced saving mechanism. Did you know that for employees aged 35 and below, the total mandatory contribution is 37% of your salary (20% from you, 17% from your employer)?

Primary Function

Ordinary Account (OA) 2.5% interest. Housing, Education, Investments

Special Account (SA) 4.0% interest. Retirement Savings, Long-term Investments

MediSave Account (MA) 4.0% interest. Healthcare, Insurance Premiums

Retirement Account (RA) 4.0% interest. Lifelong Monthly Payouts (CPF LIFE)

Data Point: As of June 2025, there are over 4.3 million CPF members with total balances amounting to over $635 billion, underscoring its role as the foundation of the nation's financial security (Source: CPF Board Statistics, 2025).

The CPF system is Singapore's answer to self-reliance. It’s a dynamic process that shifts your savings from accessible accounts (OA) in your youth to protected, high-interest accounts (SA/RA) as you move towards retirement, ensuring a roof over your head, money for medical emergencies, and a lifelong monthly income.

Disclaimer: This article is for informational purposes only and does not constitute professional financial advice.

Address

Blk 8 Cantonment Close

SIngapore