Check requirements for Asia's Retirement Visas

How can you retire in Asia with a family and $1M USD in 2026?

The expat retirement landscape is changing. Compare the new financial thresholds for Malaysia's MM2H tiers, Thailand's LTR, and the strict Talent/Family hurdles in China, India, and Japan for 2026.

GEO-ARBITRATE RETIREMENT

2/14/20264 min read

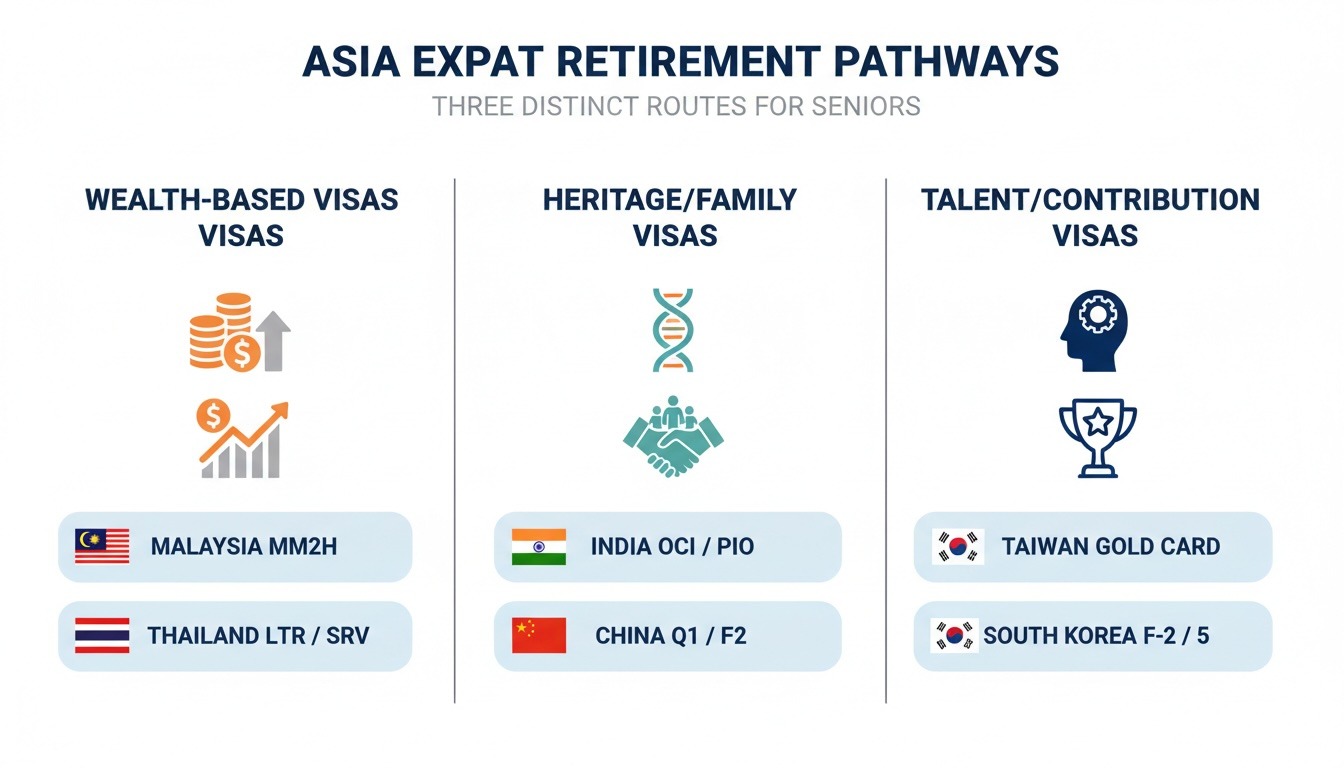

For seniors planning or seeking their long-term stay in Asia, the rules are changing. Most desirable destinations are moving away from simple, low-cost "retirement visas." The new landscape is defined by increased financial requirements, mandatory health insurance, and a strong preference for applicants with wealth or professional value.

Neither China, India, Japan, South Korea, nor Taiwan offers a straightforward passive retirement visa. Entry is reserved for those who meet high thresholds in wealth, talent, or ability to provide descent.

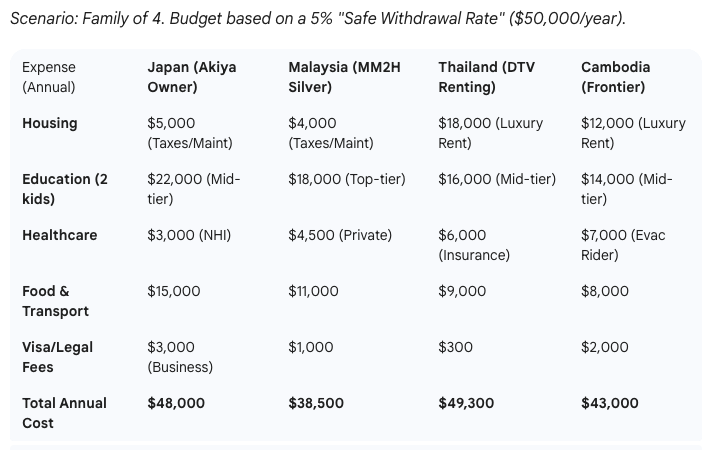

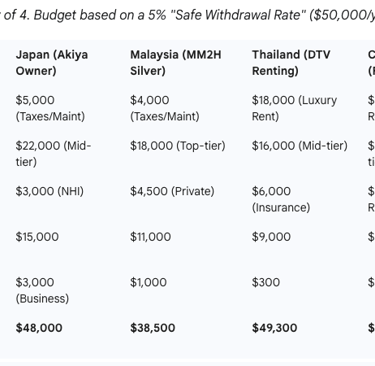

The $1M USD family retirement in Asia is the ultimate "middle-class-to-millionaire" pivot. But in 2026, the landscape has changed. Gone are the days of a $500 monthly lifestyle in a coastal hut. Today, it’s a game of Capital Efficiency: how to deploy your $1M to secure a world-class education for your kids and high-tier healthcare for your family without draining the tank.

If you have $1M, you aren't just "retiring"—you are managing a small family endowment. Here is the 2026 4 strategic blueprint towards retirement in Asia to give you a guide on your own "retirement" vision.

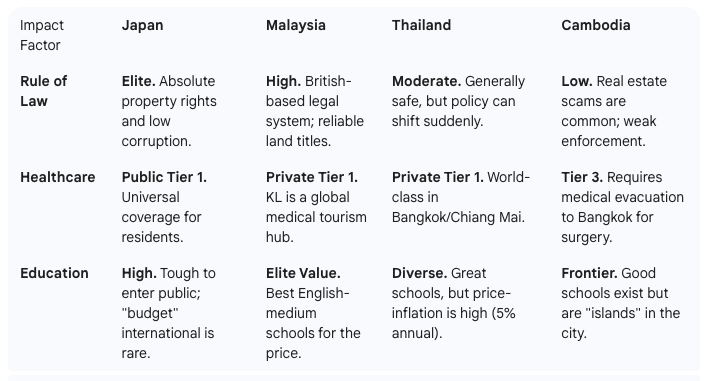

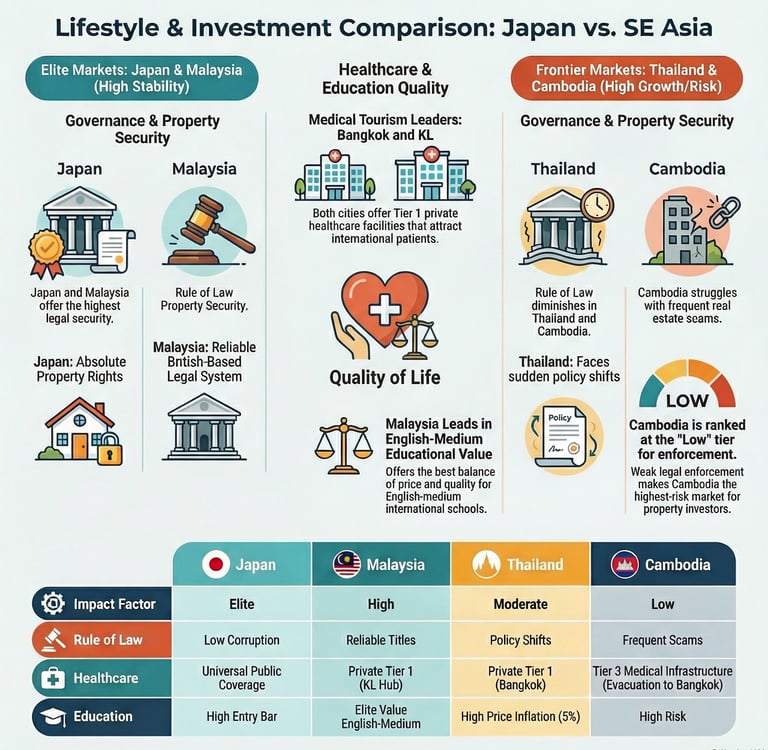

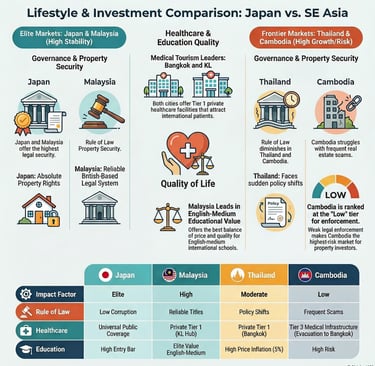

1. The Strategic Impact Study: Rule of Law & Infrastructure

Before looking at beach photos, you must evaluate the "Safety Net" of your chosen destination. For a family, the "Rule of Law" isn't just a political term—it’s the guarantee that your house won't be seized and your insurance will actually pay out.

2. The Four Strategic Pillars

The "Akiya Gambit" (Japan): Ownership at High Stability

Japan is the only "rich" country where you can buy landed property for the price of a used SUV.

The Move: Buy an abandoned Akiya in a regional city (like Fukuoka or the Izu Peninsula) for $50,000. Spend $100,000 on a "passive house" renovation.

The Visa: Since owning property doesn't give a visa, you’ll likely use the Business Manager Visa (updated 2026 requirement: ~$200k capital investment and one local hire).

Strategy: You "Anchor" $350k into Japan (House + Visa Business) and keep $650k in US stocks. Your kids go to a local school (free immersion) or a mid-tier international school.

The "English Anchor" (Malaysia): The Education Hub

Malaysia remains the "sweet spot" for families who want a Western-style life with an Asian price tag.

The Move: The Silver Tier MM2H (2026). You lock $150,000 in a fixed deposit and must buy a property (min. $135,000).

The Visa: A 5-year renewable visa for the whole family.

Strategy: English is the lingua franca. You buy a modern condo in Kuala Lumpur. Your kids attend top British-curriculum schools for $10k/year—half the price of Singapore.

The "Digital Nomad Hack" (Thailand): Maximum Liquidity

If you want to keep your $1M in the S&P 500 and not "lock" it in a foreign bank, Thailand's 2026 DTV (Destination Thailand Visa) is the cheat code.

The Move: A 5-year visa for $300 with a proof of only $15,000 in savings.

The Visa: Multiple entry, allows spouse and children under 20.

Strategy: Rent everything. You live in a luxury villa in Chiang Mai or Koh Samui. You keep your $1M liquid, earning 5-8% returns, which fully funds your lifestyle.

The "Frontier Yield" (Cambodia): High Growth, High Risk

The Move: Use the CM2H (Cambodia My Second Home).

The Visa: 10-year visa with a path to a Cambodian passport after 5 years.

Strategy: Cambodia allows 100% foreign business ownership. You invest $100k in local real estate (condos) and use the high rental yields (6-8%) to offset your family's living costs.

4. Advanced 2026 Pro Tips

A. The "Akiya" Warning

While Japan allows you to buy landed property, don't buy a house in a "Yellow Zone" (landslide/flood prone). In 2026, insurance companies are becoming more selective about rural Japanese risks. Always check the Hazard Map before signing.

B. The Education "Ladder"

If you choose Thailand or Malaysia, don't start at a Tier 1 school (e.g., ISKL or NIST) which costs $35k/year. Start at a "Tier 2" school. The facilities are 90% as good, and you save $40,000/year for two kids—enough to pay your entire rent.

C. Currency De-risking

Do not convert your entire $1M into THB, MYR, or KHR. In 2026, keep 80% in USD/EUR/SGD and only move what you need for 6 months into the local currency. This protects you from the "emerging market currency slide."

D. The 180-Day Tax Rule

In 2026, Thailand and Malaysia are cracking down on "tax residents." If you stay more than 180 days, you are technically liable for tax on income brought into the country. Strategy: Use your $1M capital for living expenses and leave your "income" (dividends/interest) in an offshore account to minimize tax exposure.

Disclaimer: This article is for informational purposes only and does not constitute professional immigration, financial or medical advice.

Address

Blk 8 Cantonment Close

SIngapore