Visa rules change all the time. Stay legal by checking requirements for Asia's Travel and Retirement Visas. Updated July 2026.

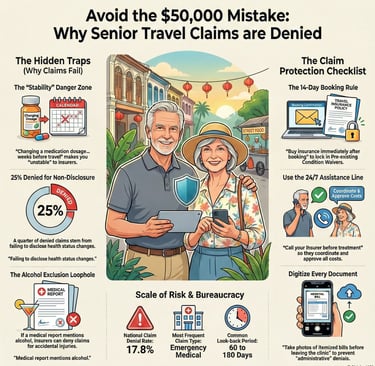

Avoid a $50,000 mistake. Why are senior travel insurance claims denied?

You’ve spent decades working, saving, and dreaming of that bucket-list trip to the cherry blossoms of Japan or the rolling hills of Chiangmai. You’ve packed your sensible shoes, your high-SPF sunscreen, and—most importantly—you’ve bought travel insurance. You’re responsible. You’re prepared. You’re practically a poster child for "Adulting."

Then, the unthinkable happens. A sudden dizzy spell in Kyoto or a stumble in Bangkok leads to a hospital visit. You file your claim, expecting a smooth reimbursement, only to receive a letter that basically says, "Thanks for the premium, but we’re not paying. Best of luck!" Navigating Thailand hospital systems.

This is serious advice. It is not a first time I hear of this. I have friends who had travel insurance rejected especially if the amount is big. There has been many media coverage on this; a 65 year old man, had a stroke, admitted to the emergency hospital while on holiday in Japan and then the daughter had her hospital claims rejected because he had high-blood-pressure but did not add a pre-existing coverage and clause to their travel insurance policy. Be sure to add pre-existing coverage the moment your health has anything on the radar, however minor.

It’s enough to make you want to throw your luggage into the nearest canal. But here’s the thing: Insurance companies aren't just being "mean." They are operating on a strict diet of definitions and data. According to a 2025 Transparency in Coverage report, claim denial rates have been climbing, with some sectors seeing denials as high as 17.8% nationally. Even more startling, a 2024 report by Squaremouth noted that emergency medical claims are now the most frequent claim type, yet "failure to disclose material facts" remains a top reason for rejection.

If you want your claim to actually get paid, you need to stop thinking like a traveler and start thinking like an underwriter. Here are the 5 phrases that are essentially "kryptonite" for your insurance payout—and how to rephrase your reality to protect your wallet.

1. "It’s just a minor check-up."

To you, a quick visit to the doctor last month for a "fluttery heart" was just a routine precaution. To an insurance company, that is a Pre-existing Condition.

The Trap: Most senior policies have a "look-back period" (usually 60 to 180 days). If you sought medical advice, changed medication, or even had a symptom—even if you weren't officially diagnosed—it’s considered pre-existing.

How to avoid it: Always purchase a Pre-existing Condition Waiver within 14–21 days of making your initial trip deposit. This "magic" clause forces the insurer to ignore your medical history.

2. "I’ve been feeling a bit off lately."

In the insurance world, the word "Stable" is king. If your health hasn't been "stable" for the duration of the look-back period, you are in the danger zone.

The Trap: If your doctor adjusted your blood pressure medication dosage three weeks before your trip, you are no longer "stable" in the eyes of the insurer.

The Stats: According to 2024 industry data, nearly 25% of denied claims stem from a failure to disclose a change in medical status.

How to avoid it: If your meds change, call your insurer immediately to update your policy. Don’t wait until you’re in an ambulance in Seoul (서울).

3. "The hospital said I should stay, but..."

Ignoring Medical Necessity is a fast track to a $0 payout.

The Trap: If you decide to fly home against medical advice (AMA) or choose a more expensive "private" hospital when a standard one was available and adequate, the insurer may deny the "excess" costs.

How to avoid it: Always call your insurance provider's 24/7 Assistance Line before agreeing to major treatments or changing your travel plans. Let them coordinate the care so they are on the hook for the bill.

4. "I didn't think I needed the receipt for that."

In the digital age, "take my word for it" doesn't fly. Incomplete Documentation is the leading cause of "administrative" denials.

The Trap: Insurers require the final itemized bill, not just the credit card receipt or an "interim" invoice.

How to avoid it: Use your smartphone to take photos of every single document before you leave the hospital or clinic. If it’s in a local language, like Thai (ไทย), ask for an English version immediately; it’s much harder to get one once you’ve flown home.

5. "I had a glass of wine with dinner."

The Alcohol Exclusion is the "gotcha" that catches many seniors off guard.

The Trap: Many policies have a clause that denies coverage if an injury occurs while you are "under the influence." You don't have to be falling-down drunk; if the medical report mentions alcohol, the insurer has a loophole to jump through.

How to avoid it: If you’ve had a mishap, be very careful about how the incident is recorded. If you tripped because of an uneven sidewalk, make sure the medical report says "uneven sidewalk," not "patient appeared intoxicated after dinner."

Your Step-by-Step Claim Protection Checklist

The 14-Day Rule: Buy your insurance as soon as you book the trip to lock in pre-existing condition waivers.

Define "Stable": Ask your doctor: "Has my treatment plan changed in the last 90 days?" If yes, disclose it.

Phone First: Save your insurer’s international emergency number in your contacts.

Paper Trail: Keep a digital folder of every receipt, medical note, and police report.

Ready to travel with total peace of mind? Before you head to the airport, double-check your policy's "Exclusions" page. It’s not the most exciting beach read, but it’s the only one that could save you $50,000.

As a senior, there are also other insurance traps you need to be aware of. One of them is critical illness claims. Read about my challenges claiming for my sudden stroke.

What are the common essential travel apps you should have if you travel in Asia.

Leave a comment below: Have you ever had a claim denied? Tell us your story so others can learn from your experience!

Disclaimer: This article is for informational purposes only and does not constitute professional advice.

Address

Blk 8 Cantonment Close

SIngapore