Check requirements for Asia's Retirement Visas

What Is a Legacy Portfolio — And Why Every Retiree Over 60 Needs One

A legacy portfolio is the portion of your retirement savings you never intend to spend. It grows quietly in the background, invested for the long term, and becomes the most meaningful financial decision most retirees never make deliberately. Here's what it is, how it works, and how to set one up.

RETIREMENT PLANNING

6/2/20265 min read

Most retirement planning conversations are built around one question: will you run out of money?

It is an important question. But it quietly assumes that the goal of retirement finance is simply to survive to the end — to cross the finish line with the accounts not quite at zero. For a growing number of people, that framing is too narrow. And the financial concept that's starting to change it is called the legacy portfolio.

Before we get into the detail — here's a clear overview from Charles Schwab on why legacy planning is worth building into your retirement thinking now, not later:

What a Legacy Portfolio Actually Is

A legacy portfolio is a defined portion of your retirement savings that you set aside with a specific intention: it is not for you to spend.

Not a backup emergency fund. Not the money you'll tap if the markets turn. A deliberate, separated allocation — invested for the long term — that will eventually transfer to whoever or whatever matters most to you. Your children. Your grandchildren. A cause you believe in. A combination.

The crucial distinction is intention. Most people have some assets they don't expect to spend in their lifetime. The difference with a legacy portfolio is that you make that explicit — you give it a clear purpose, invest it accordingly, and plan for how it will transfer.

That shift in framing changes everything about how the money is managed.

Why the Time Horizon Is Longer Than You Think

Here is the part most people don't initially appreciate.

If you are 63 years old today and your beneficiary is your 35-year-old child, the money in your legacy portfolio doesn't need to perform for your remaining 20 or 30 years. It needs to perform across both lifetimes — potentially 50 or 60 years from now.

That is an extraordinarily long runway. And on that runway, the conventional conservative portfolio recommended for retirees — heavily weighted toward bonds and cash — is almost certainly the wrong vehicle.

Money you will genuinely never spend can afford to take more risk, because it has time to recover. Growth assets — broadly diversified equities, index funds, real estate investment trusts — that would feel uncomfortable for your day-to-day retirement income become entirely appropriate when the true investment horizon is the next generation.

This is why legacy portfolios are worth separating from your retirement income strategy. Not because they're complicated. But because they should be managed differently.

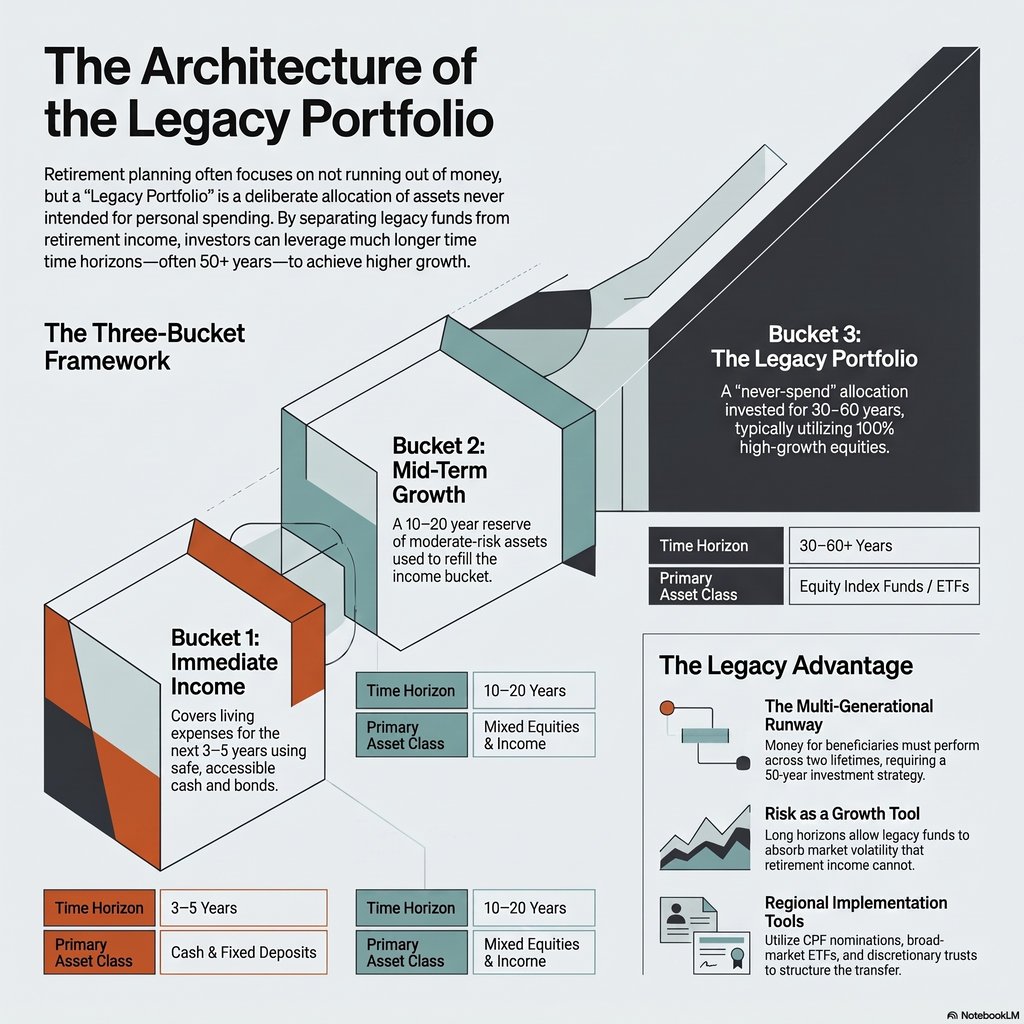

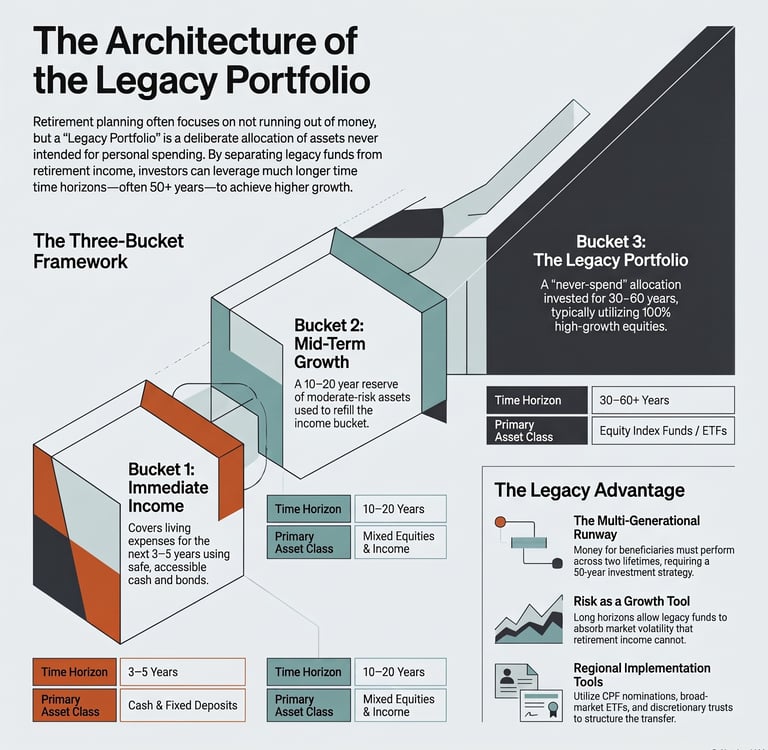

The Three-Bucket Framework

A simple way to think about retirement assets once you're in your 60s:

Bucket 1 — Income (spend now): Covers living expenses for the next 3–5 years. Cash, fixed deposits, short-term bonds. Safe, accessible, boring by design.

Bucket 2 — Growth (spend later): The longer-term retirement reserve. A mix of equities and income assets that refills Bucket 1 over time. Moderate risk. 10–20 year horizon.

Bucket 3 — Legacy (never spend): Your legacy portfolio. Invested for growth over the longest possible horizon. Could be 100% equities or equity index funds if your time horizon is 30–50 years. This bucket has a completely different job to the other two — and should be treated accordingly.

The size of Bucket 3 doesn't need to be defined by any particular number. Some people ring-fence 10% of their assets. Others ring-fence whatever is left after funding Buckets 1 and 2 comfortably. The exact allocation matters less than the deliberate act of separating it.

How to Structure It in Asia

For readers in Singapore, Malaysia, Thailand, or elsewhere in the region, there are a few practical considerations worth knowing.

In Singapore, CPF savings can be nominated to specific beneficiaries through the CPF nomination system — and this operates outside of your will, which means it transfers directly and quickly. If you haven't made a CPF nomination, or if yours is outdated, reviewing it is one of the highest-return administrative tasks you can do this month.

Beyond CPF, the tools most relevant for legacy portfolios in Asia include:

Broad-market equity ETFs — available through most brokerage accounts in Singapore, Malaysia, Hong Kong. Low-cost, globally diversified, and appropriate for a long horizon.

Unit trusts and REITs — accessible through banks and platforms like Endowus, StashAway, or local bank advisory services.

Whole life insurance with investment components — widely used in the region for legacy transfer. Worth reviewing for costs and actual legacy value versus term + invest alternatives.

Discretionary trusts — for larger estates, or where structured distribution across multiple beneficiaries or generations is preferred. A trust lawyer familiar with your jurisdiction is the right person to advise on this.

None of this is complicated to set up. What it requires is the decision that a legacy portfolio is worth having — and then a conversation with a licensed financial planner to match the structure to your actual situation.

What If You're Not Sure You Have Enough to Think About Legacy?

This is the objection most people raise, and it deserves a direct answer: you don't need to be wealthy to have a legacy portfolio.

If you have retirement savings beyond what you confidently expect to spend — any amount — the question of what happens to it is worth answering deliberately. Without that intention, the money typically disperses in ways that were never planned, after delays and processes that could have been avoided.

Equally important: a legacy portfolio doesn't have to be about money at all. For many people, the most meaningful legacy is a clear, documented plan — who gets what, under what conditions, guided by what values. That documentation costs almost nothing and provides enormous clarity for the people left to handle it.

The financial piece compounds over time. The clarity piece starts working the day you write it down.

The Bottom Line

Retirement planning has traditionally been about making sure you're okay. A legacy portfolio asks a slightly different and ultimately more interesting question: what do you want to still be doing after you're gone?

It doesn't require a large estate. It doesn't require a lawyer on retainer (though some of what you build may eventually involve one). It requires the decision to treat a portion of your assets as belonging to the future — and then managing them accordingly.

If you haven't yet thought through the broader picture of how to structure income and growth in retirement, our guide on retirement income strategies is the right place to start before thinking about legacy. And since the lifestyle you build in retirement shapes how much you actually spend — and therefore how much eventually passes on — the question of whether to move overseas as a retirement strategy is worth considering alongside the financial planning.

Eat well, move well, and build something worth leaving behind. They're not separate goals.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, legal, or investment advice. The financial landscape varies significantly by country. Always consult a licensed financial planner or estate attorney in your jurisdiction before making decisions about retirement assets, estate planning, or investment allocation.

Address

Blk 8 Cantonment Close

SIngapore